Mileage is one of the most misunderstood pricing factors in auto insurance. Many drivers know it matters, but few understand how insurers evaluate mileage, why it affects risk calculations, and how to use it strategically to lower premiums.

This guide explains, in practical and non-theoretical terms, how annual mileage influences insurance rates, what mileage thresholds insurers use, and how you can optimize your policy in 2026 and beyond—without misrepresentation or coverage risk.

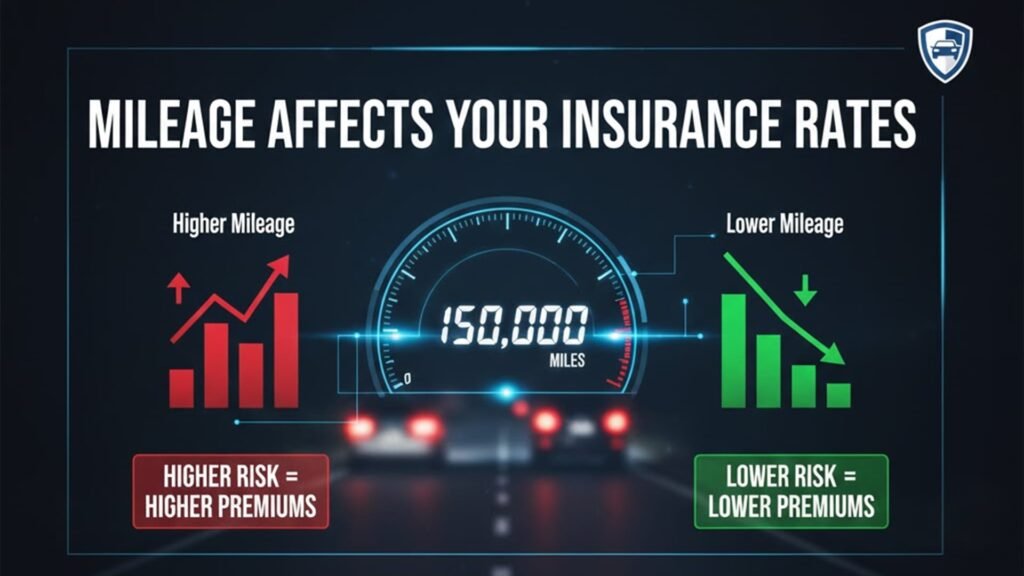

Why Mileage Matters to Insurance Companies

From an insurer’s perspective, mileage is simple: the more you drive, the more exposure you create.

Insurance pricing is built on probability. Each mile increases the likelihood of:

- Collision involvement

- Liability claims

- Physical damage losses

- Comprehensive claims (debris, animals, road hazards)

Mileage is therefore a direct risk multiplier, not a vague behavioral signal.

Table: Typical Mileage Bands Used in Insurance Rating

| Annual Mileage | Risk Classification | Premium Impact |

|---|---|---|

| Under 5,000 miles | Very Low | Significant discounts |

| 5,000–7,500 miles | Low | Moderate discounts |

| 7,500–12,000 miles | Average | Baseline pricing |

| 12,000–15,000 miles | Above Average | Slight increase |

| 15,000–20,000 miles | High | Noticeable increase |

| Over 20,000 miles | Very High | Maximum surcharge |

Important: Mileage thresholds vary by insurer, state, and underwriting model, but these ranges are widely used across the industry.

How Insurers Verify Your Mileage

Contrary to popular belief, insurers do not rely solely on trust.

Common Verification Methods

- Odometer readings at policy start or renewal

- State inspection and registration data

- Claims records showing usage patterns

- Telematics and usage-based insurance (UBI) programs

Why Accuracy Matters

Underreporting mileage can result in:

- Policy repricing at renewal

- Claim disputes

- Coverage denial in extreme cases

Accuracy protects both your premium and your claim eligibility.

Low Mileage vs. High Mileage Drivers: Real Cost Differences

Low-mileage drivers statistically file fewer claims and generate lower total losses.

Low Mileage Profiles

- Remote workers

- Retirees

- Urban residents using public transport

High Mileage Profiles

- Long-distance commuters

- Sales and field professionals

- Rideshare or delivery drivers (often require commercial coverage)

Insurers price accordingly.

Mileage vs. Driving Behavior: What Matters More?

Mileage measures how often risk occurs. Driving behavior measures how well you manage it.

That distinction explains why usage-based insurance exists.

When Behavior Can Offset Mileage

- Smooth braking

- Consistent speed control

- Low night-time driving

A high-mileage but low-risk driver can sometimes pay less than a low-mileage aggressive driver.

Usage-Based Insurance (UBI): Mileage-Based Pricing in Practice

Usage-based insurance programs directly link premiums to mileage and behavior.

How UBI Programs Work

- Smartphone apps or onboard devices track miles driven

- Safe driving habits earn dynamic discounts

- Premiums adjust based on actual usage, not estimates

Who Benefits Most

- Drivers under 10,000 miles annually

- Predictable commute patterns

- Defensive drivers

For the right driver, UBI can reduce premiums by 10–30%.

How to Lower Your Insurance Premium by Managing Mileage

Mileage reduction does not require lifestyle overhauls.

Practical, Sustainable Strategies

- Combine errands into fewer trips

- Use remote or hybrid work options when available

- Carpool for commuting

- Avoid unnecessary short trips

- Accurately update mileage when habits change

Even a reduction of 2,000–3,000 miles per year can move you into a lower pricing tier.

Common Mileage Myths That Cost Drivers Money

“Mileage Doesn’t Matter If I’m a Safe Driver”

False. Safety helps, but exposure still drives pricing.

“Insurers Can’t Verify Mileage”

Incorrect. Data sources are increasingly interconnected.

“Once Set, Mileage Never Changes My Rate”

Wrong. Mileage is reviewed at renewal and after claims.

Special Cases: When Mileage Matters Even More

New Drivers

Higher mileage amplifies inexperience risk.

Luxury and Performance Vehicles

Each mile costs more to insure due to repair expenses.

Rideshare and Delivery Use

Personal policies often exclude commercial mileage.

Failing to disclose these use cases can invalidate coverage.

Frequently Asked Questions

Does low mileage always mean lower insurance?

Generally yes, but only when accurately reported and verified.

Is mileage more important than location?

Location often outweighs mileage, but mileage remains a major modifier.

Can I update my mileage mid-policy?

Most insurers allow updates, especially after lifestyle changes.

Final Verdict: Mileage Is One of the Few Factors You Can Control

You can’t change your age, zip code, or past claims—but you can manage how much you drive and how accurately you report it.

For drivers focused on long-term savings, mileage awareness is not optional—it’s strategic. Understanding how insurers interpret mileage gives you leverage, pricing transparency, and better coverage decisions.

Drive less, report accurately, and price smarter.

Useful Links: